For extra insights into stablecoin market dynamics, you may additionally be excited about our previous report analyzing illicit exercise patterns in USDT and USDC transactions.

1.Summary

2.Scope of Analysis

On this report the next three prime steady cash are analyzed: USDT, USDC and BUSD. Particularly:

- Historical past, Transacting Volumes and Customers.

- Timeline of Statistics Alongside With Some Key Dates.

- Utilization Patterns and Flows Between Main Varieties of Brokers.

- Prospects of Journey Rule Enforcement for Funds in Steady Cash.

3.Definitions

3.1. Steady Coin

A stablecoin is a sort of cryptocurrency designed to have a steady worth. This steady worth is often pegged to a reserve or benchmark, akin to a certain quantity of a commodity (like gold) or extra generally, a fiat foreign money (just like the US greenback). The first goal of stablecoins is to offer the advantages of digital foreign money – akin to quick transactions, privateness, and safety – with out the excessive worth volatility sometimes related to cryptocurrencies. There are a number of mechanisms used to attain this stability:

- Fiat-Collateralized Stablecoins: These are backed by a reserve of fiat foreign money, sometimes held in a financial institution or a trusted third-party. For each stablecoin issued, there’s a corresponding unit of fiat foreign money held in reserve. Examples embrace USDC and Tether (USDT) and BUSD.

- Crypto-Collateralized Stablecoins: These are over-collateralized by different cryptocurrencies, akin to Ether. If the worth of the collateral drops, mechanisms are triggered to make sure the stablecoin’s worth stays steady. A well-liked instance is DAI, which operates on the Ethereum platform.

- Algorithmic Stablecoins: These should not backed by collateral however as an alternative use algorithms and good contracts to robotically modify the availability of the stablecoin, rising or reducing it in response to modifications in demand to keep up its peg. Examples embrace Ampleforth (AMPL) and Terra (LUNA).

3.2. Steady Coin Collateral

Collateral is a reserve of fiat foreign money, sometimes held in a financial institution or a trusted third-party. Is also cash surrogates, Bonds, Treasuries, typically even shares of firms following inventory market indexes (like Vanguard (VOO) for SNP500).

3.3. Steady Coin Depeg

On this analysis we’ll be analyzing the fiat-collaterized steady cash. Depeg is an occasion when stablecoin market worth deviates from the fiat foreign money they’re pegged to, usually as a result of elements akin to:

- Doubts Concerning the Precise Reserve Backing

- Mismanagement by the Issuing Entity

- Regulatory Pressures

- Sudden, Massive Redemption Requests.

In such eventualities, if merchants consider that the stablecoin would not actually have a 1:1 fiat reserve as claimed, or if they believe they could face challenges redeeming the stablecoin at its full worth, they could unload their holdings, main the stablecoin’s worth to drop beneath its meant peg.

3.4.Steady Coin Holder

Holder is an individual or a sensible contract which “holds” some quantity of Stablecoins on its tackle. Holder can transact in Stablecoins with different Holders.

3.5.Centralized Trade (CEX)

A centralized alternate is a platform the place customers can purchase, promote, or commerce cryptocurrencies and, in some instances, fiat currencies. Key traits of centralized exchanges embrace:

- Custodial: Centralized exchanges maintain customers’ funds, both in fiat or cryptocurrency, of their custody. Once you deposit funds right into a centralized alternate, you are basically entrusting them with the safekeeping of your property.

- Consumer Accounts: To commerce on a centralized alternate, customers sometimes need to create an account and bear a Know Your Buyer (KYC) verification course of, which entails offering private particulars to adjust to rules.

- Order Books: These platforms use order books to match consumers and sellers. Customers place market or restrict orders, that are then matched by the alternate’s buying and selling engine.

- Interface: Centralized exchanges usually present user-friendly interfaces, charting instruments, and different buying and selling sources, making it simpler for each novice and skilled merchants.

- Liquidity: Because of their recognition and consumer base, centralized exchanges usually have excessive liquidity, making it simpler to execute giant trades with out considerably affecting the market worth.

- Charges: Centralized exchanges sometimes cost charges for trades, deposits, or withdrawals. The price construction can fluctuate primarily based on the platform and the consumer’s buying and selling quantity

- Safety: Whereas CEXs implement strong safety measures to guard consumer funds and knowledge, they’ve been targets of hacks previously. As a centralized level of failure, they are often extra susceptible than decentralized methods.

Examples of widespread centralized exchanges embrace Binance, Coinbase, Kraken, and Bitfinex.

3.5.1. CEX Sizzling Pockets

Sizzling pockets is an tackle the place CEX entity retains its Steady Cash (liquidity) obtainable for speedy withdrawal by customers. From the enterprise perspective, CEX makes use of Sizzling Pockets to service speedy customers withdrawal and collects deposits onto this tackle. This pockets is often built-in with CEX data methods for enterprise operation functions and thus might be compromised in occasion when the knowledge system is compromised, leading to funds draining by hackers.

3.5.2. CEX Consumer Deposit Handle

Due to the truth that a cost (or switch) in StableCoin doesn’t have “cost description” discipline, there isn’t any manner for CEX to tell apart between completely different customers depositing their Stablecoins. To mitigate this subject, CEX creates a so-called “Consumer Deposit Handle”, which is actually a personalised distinctive tackle devoted to just accept stablecoins from precise one consumer. This basically leads to a truth, that CEX makes use of not a single pockets customers transact with, however a lot of wallets for various functions.

3.6.Decentralized Trade

A decentralized alternate (DEX) is a cryptocurrency buying and selling platform that operates with out a government or middleman. As a substitute of counting on a centralized entity to facilitate trades, DEXs use blockchain expertise, primarily within the type of Sensible Contracts, to robotically match purchase and promote orders. Key traits of decentralized exchanges embrace:

- Non-Custodial: DEXs don’t maintain or have custody of customers’ funds. As a substitute, trades are made immediately from one consumer’s pockets to a different.

- No KYC: Most DEXs do not require customers to bear a Know Your Buyer (KYC) verification course of, guaranteeing better privateness and anonymity.

- Sensible Contracts: DEXs depend on good contracts to facilitate and confirm trades. This automation ensures that the phrases of the commerce are executed exactly as agreed upon.

- Liquidity: Early DEXs confronted challenges associated to low liquidity, making it more durable to execute giant trades. Nonetheless, the introduction of liquidity protocols and swimming pools, like these utilized in Uniswap or SushiSwap, has addressed a few of these issues.

- Interoperability: Some DEXs are designed to be interoperable, permitting for trades throughout completely different blockchains or networks.

- Charges: DEXes additionally could cost charges from every commerce, however customers additionally need to pay “fuel charges” individually for the execution of good contracts on the blockchain community, particularly on platforms like Ethereum. Which makes utilization of DEXes dearer in comparison with CEXes.

- Consumer Expertise: Initially, DEXs had been seen as much less user-friendly in comparison with centralized exchanges. Nonetheless, with the evolution of the DeFi (Decentralized Finance) ecosystem, many DEX platforms have develop into extra intuitive and user-centric.

Examples of widespread decentralized exchanges embrace Uniswap, SushiSwap, PancakeSwap, and Balancer.

4.Historic Overview of Main Fiat-Collateralized Stablecoins

4.1.Historic Overview

4.1.1.USDT (Tether USD)

– 2014-2015: Start and Early Days

Tether was initially conceived in a whitepaper titled “The Mastercoin white paper” by J.R. Willett in January 2012. The implementation of Tether on the Mastercoin protocol turned the predecessor to the Omni Layer, a platform for creating and buying and selling customized digital property on the Bitcoin blockchain. Tether was launched in July 2014 as “Realcoin” by Brock Pierce, Reeve Collins, and Craig Sellars. A short time later, it rebranded as “Tether” and launched the USDT ticker. The first proposition was easy – each USDT token was presupposed to be backed by one US greenback held in reserve. This 1:1 peg was designed to mix the steadiness of the U.S. greenback with the technological benefits of cryptocurrency.

–2016-2017: Adoption and Controversy

Tether started to be built-in into a number of distinguished cryptocurrency exchanges, like Bitfinex, which led to elevated adoption and use. Issues started to come up relating to whether or not Tether truly held sufficient U.S. {dollars} to again all USDT in circulation. Moreover, the shut relationship between Bitfinex and Tether (they share key executives) was spotlighted, notably after points associated to banking entry and wire transfers.

–2018: Intense Scrutiny and Authorized Battles

Tether’s banking relationships got here beneath the highlight. Initially, Tether had difficulties with banking partnerships, shifting from one financial institution to a different. The group grew extra skeptical about Tether’s greenback reserves. Though Tether claimed each USDT was backed by a greenback, they discontinued relationships with auditors earlier than a full audit might be offered.

– 2019-2020: Authorized Investigations and Partial Backing Admission

NYAG Investigation: The New York Legal professional Common (NYAG) started investigating Bitfinex and Tether, suggesting {that a} cover-up had taken place to cover a lack of funds.

Backing Admission: Tether modified its claims in 2019, stating that USDT was not solely backed by money but additionally by “money equivalents” and “different property and receivables from loans.”

–2021 and Past:

Authorized Settlement: In 2021, Tether and Bitfinex settled with the NYAG, agreeing to pay $18.5 million in damages and being clear about reserves. They didn’t admit to any wrongdoing.

4.1.2. Present State

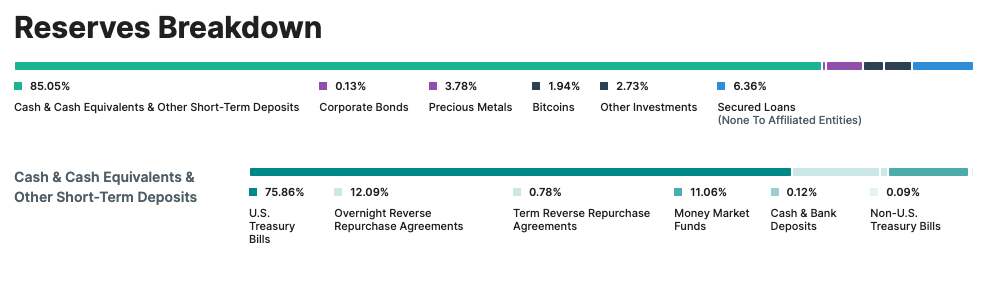

Reserves: Based on newest report (dated June 30, 2023), Tether reserves are distributed the next manner:

- Treasury Payments: 75,86%

- In a single day Reserve: 12,09%;

- Market Funds: 11,06%;

- Secured Loans: 6,36%;

- Bitcoins and Different Investments: 4,76%

- Company Bonds, Funds & Valuable Metals: 3,91%.

Whole Emission: 86,6B USDT

Supported Blockchains:

- Ethereum (emission 39B USDT)

- Tron (emission 43,8B USDT)

- Binance chain (emission 3,37B USDT)

- Different Blockchain (with comparatively low emission)

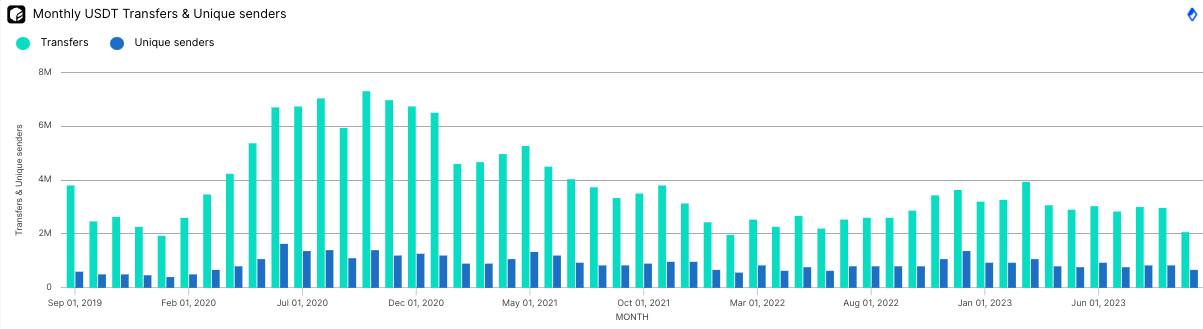

Transaction and Volumes:

- A major spike in transferred quantity is seen round Dec 2020-Jan 2021, in the beginning of the Bitcoin bull run. This might point out extra capital was flowing into the market, with traders probably hedging with USDT.

- Publish-Nov 2022, transferred quantity sees a decline and stays subdued. This will recommend lowered market exercise, even with a slowly rising BTC worth, indicating uncertainty in regards to the market’s route.

- In abstract, the rise of DeFi period and consequently the Bitcoin bull run noticed elevated USDT transfers and quantity, indicating heightened market exercise and maybe hedging, the bear market has led to constant but subdued USDT exercise, reflecting market uncertainty and warning amongst merchants.

- Transfers and distinctive senders surged round Feb 2020. This aligns with the onset of the DeFi period, suggesting elevated adoption and exercise in DeFi platforms.

- A noticeable decline in each metrics happens after Could 2021, through the center of the bitcoin bull run. This might be as a result of customers held on to their property anticipating larger returns.

- Publish-Nov 2022, through the bear market’s deep dive, each transfers and distinctive senders stay comparatively steady, suggesting that even with declining BTC costs, USDT exercise remained constant, probably as a protected haven for capital or due to the place of USDT in enterprise actions that doesn’t rely upon BTC worth an not associated to buying and selling and hypothesis.

4.1.3. Abstract

The numerous enhance of USDT utilization in Ethereum Blockchain is matching the rise of the DeFi period, when USDT turned probably the most used base asset to commerce crypto property with.

The truth that USDT actions stay constant throughout Bitcoin low volatility time and bear market means that USDT has extra utilization somewhat than being only a base asset for buying and selling on DEXes.

5.Stablecoin Flows Between Main Agent Sorts

5.1. Scope Definition

For this specific analysis, we’ll analyze the flows between CEXes, DEXes and Holder wallets. We’ll attempt to separate switch operations primarily based on transaction sorts that are dictated by the Ethereum structure and technical choices that founders use to construct DEXes with. This may enable to separate no less than 2 varieties of transactions thus separating site visitors and cash flows. For functions of this analysis, we’ll be individually analyzing USDT in Tron and Ethereum blockchains as a result of the truth that they’ve comparable emission, however completely different utilization patterns. Regardless of the identical identify, USDT in Ethereum and Tron should not immediately interoperable and require bridging to transform one to a different, which is nothing completely different from exchanging one token to a different on alternate.

5.2. Technical Particulars

5.2.1 ERC20 Token Contract

Every stablecoin coated on this analysis is applied in a type of a Sensible Contract following the ERC20 standard and deployed in a specific EVM suitable blockchain. This commonplace defines the capabilities that consumer (Holder) could use to provoke transfers in addition to a listing of Occasions (logs) which might be recorded when such a switch has occurred. Particularly, it defines 2 capabilities that switch could also be initiated with:

perform switch(tackle _to, uint256 _value) public returns (bool success)

perform transferFrom(tackle _from, tackle _to, uint256 _value) public returns (bool success)

Within the context of this analysis, it’s necessary to say that perform “switch” is used when consumer A is initiating a transaction from his account to consumer B, i.e. sending his/her tokens on to Consumer B. Such a switch is often referred to as “Direct switch”. In contrast to the primary perform, the second (“transferFrom”) is used when a Consumer A desires to switch tokens of Consumer B to a different account (often his personal), i.e. Consumer A is charging some quantity of tokens from Consumer B’s account. This perform is often used when a Sensible Contract desires to cost Consumer for tokens, which is precisely what occurs when Consumer is transacting with DEX. These 2 several types of switch initiation permits for separation of all of the site visitors of stablecoins into Direct Transfers and Fees. First kind is used when individuals work together with one another or with CEXes, the second is used when individuals work together with a decentralized platform (DEXes, Bridges, different DeFi platforms).

5.2.2. Token Requirements in Different Blockchains

Token requirements in numerous blockchain could (and often) differ. However for functions of this analysis, we’ll be referring to the TRC20 commonplace in Tron blockchain and BEP20 commonplace in Binance chain, which are actually a replica of ERC20 commonplace in Ethereum.

5.2.3. Handle Labels

We’ll be referring to a set of tackle labels publicly obtainable on analysis platforms like https://flipsidecrypto.xyz/ and blockchain explorers (https://etherscan.io, https://bscscan.com, https://tronscan.io). These labels embrace CEX Sizzling Wallets, DEX swimming pools, routers and different well-known public addresses.

5.3. USDT CEX and DEX flows in Ethereum

For functions of this analysis we’ve analyzed USDT token utilization in 2 dimensions:

- By Vacation spot Handle (which permits to grasp out and in flows to CEXes and DEXes)

- By Switch Initiation Perform Sort (which permits to grasp precise kind of operation carried out)

- The Dataset Used Accommodates Transactions From Oct 2022 to Oct 2023. (1 12 months)

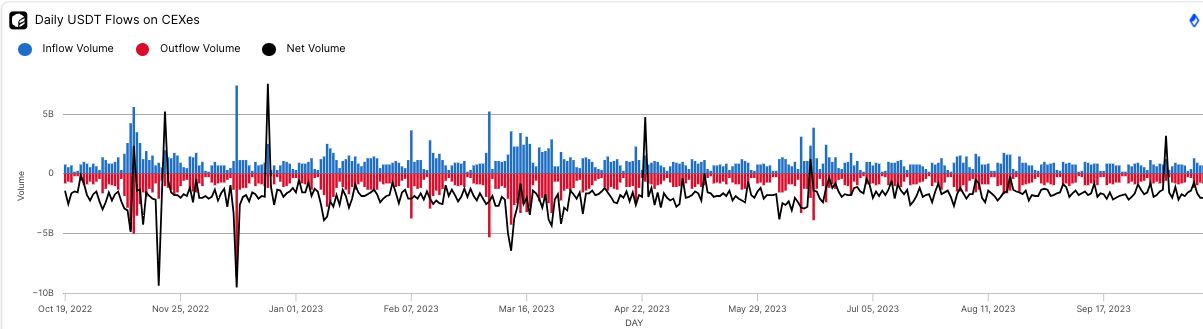

5.3.1.USDT CEX In/Out flows in Ethereum

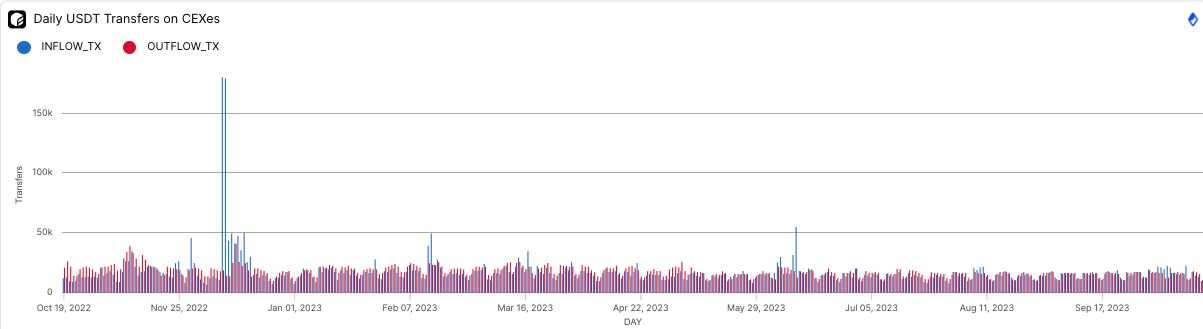

Day by day USDT Flows on CEXes (Quantity):

- Influx Quantity (Blue Bars): Represents the quantity of USDT transferred from customers to CEXes.

- Outflow Quantity (Purple Bars): Represents the quantity of USDT transferred from CEXes to customers.

- Internet Quantity (Black Line): Signifies the distinction between influx and outflow volumes. Optimistic values present extra influx than outflow, and unfavorable values present extra outflow than influx.

Day by day USDT Transfers on CEXes (Variety of Transactions):

- Influx Transactions (INFLOW_TX – Blue bars): Represents the variety of transactions constructed from customers to CEXes.

- Outflow Transactions (OUTFLOW_TX – Purple bars): Represents the variety of transactions constructed from CEXes to customers.

Key Observations (Chronologically)

- Finish of Nov 2022:

- A major spike in influx quantity.

- Correspondingly, there is a main rise within the variety of influx transactions.

- This exercise would possibly relate to anticipation of market actions following Bitcoin’s “double” prime bull run in Nov 2021.

- Mid-March 2023:

- Noticeable spike in each influx and outflow volumes.

- Elevated exercise within the variety of influx transactions.

- This correlates with the USDC 12% depeg occasion, which triggered panic gross sales available in the market.

- Early June 2023:

- One other spike in influx quantity.

- Elevated exercise within the variety of influx transactions.

- This era matches the USDT 3% depeg occasion.

- Common Observations:

- More often than not, the online quantity stays comparatively steady, indicating a balanced influx and outflow.

- Outflow transaction counts are constant all through the interval with solely minor fluctuations.

- These observations present the response of USDT transfers to and from CEXes throughout particular occasions within the cryptocurrency market.

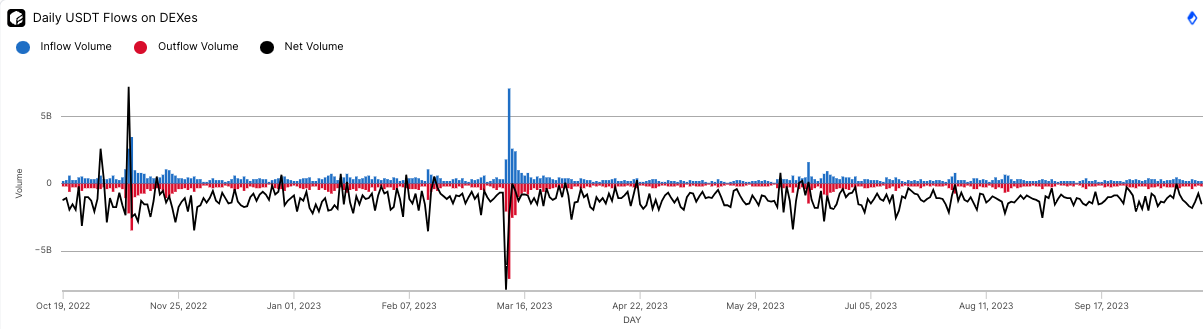

5.3.2. USDT DEX In/Out flows in Ethereum

Day by day USDT Flows on DEXes:

- Influx Quantity (Blue): The quantity of USDT transferred from customers to DEXes.

- Outflow Quantity (Purple): The quantity of USDT transferred from DEXes again to customers.

- Internet Quantity (Black): The online change in quantity on DEXes. It is the distinction between influx and outflow.

Day by day USDT Transfers on DEXes:

- Influx Transactions (Blue): The variety of transaction occasions the place USDT is moved to DEXes.

- Outflow Transactions (Purple): The variety of transaction occasions the place USDT is moved from DEXes to customers.

Key Observations:

It’s necessary to notice that Internet Quantity (Black) is unfavorable more often than not. This means that customers are tending to exit (promoting property) into USDT and fixing income on this steady coin. Likewise, the down spike on Mar thirteenth signifies that customers had been speeding out of USDC into steady USDT in a panic promote.

- Finish of November 2022:

- Vital spike in USDT influx quantity to DEXes.

- Corresponding surge in influx transaction counts.

- Optimistic Internet Quantity (Black) peak at the moment corresponds to prevailing “Shopping for” property operations somewhat than promoting.This corresponds to lowest Bitcoin worth through the newest bear market.

- Mid-March 2023:

- Distinctive spike in USDT influx quantity.

- Subsequent sharp decline in outflow quantity.

- Unprecedented peak in influx transaction counts.

- This exercise is intently aligned with the March 10-11, 2023 USDC 12% depeg occasion, suggesting a relation or response to the occasion.

- Early June 2023:

- Noteworthy influx quantity spike.

- Elevated influx transaction counts.

- This era coincides with the June 15, 2023 USDT 3% depeg occasion, hinting at a possible correlation.

- Outdoors these main occasions, influx and outflow are typically balanced by way of each quantity and transaction counts.

The timing and magnitude of those spikes, particularly across the USDC and USDT depeg occasions, recommend that customers might need been reacting to market situations by actively buying and selling on DEXes that are able to closing orders instantly evaluating to order ebook primarily based CEXes that are additionally prone to have their buying and selling API “overloaded” throughout peak volatility time.

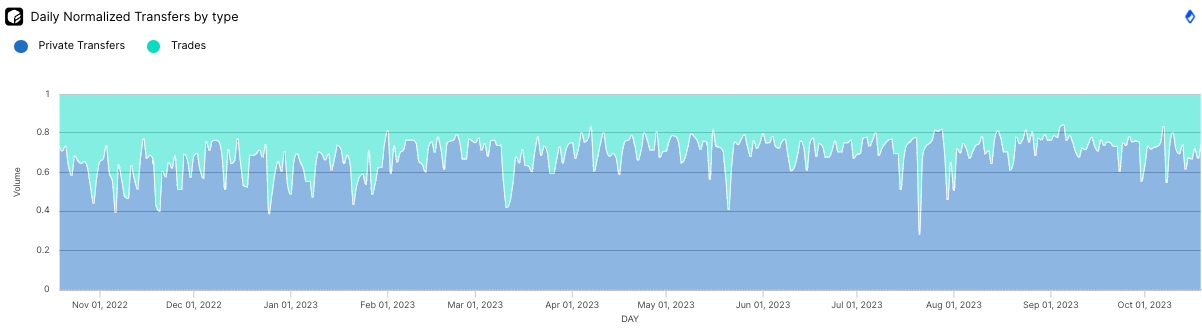

5.3.3.USDT Switch sorts evaluation in Ethereum

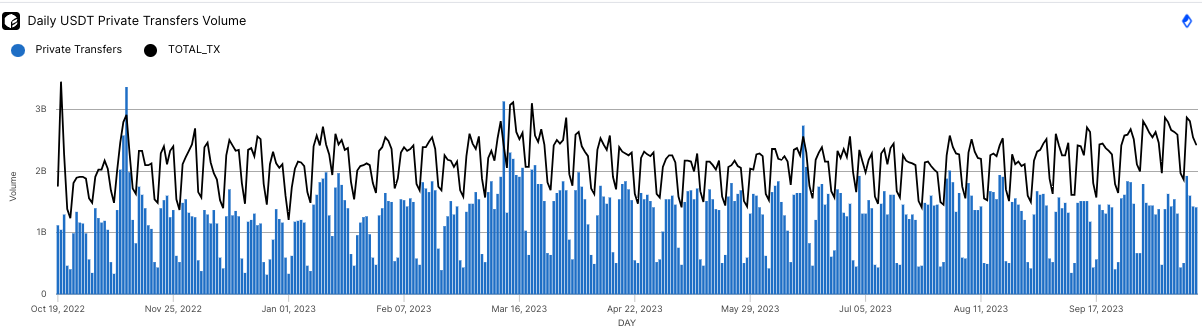

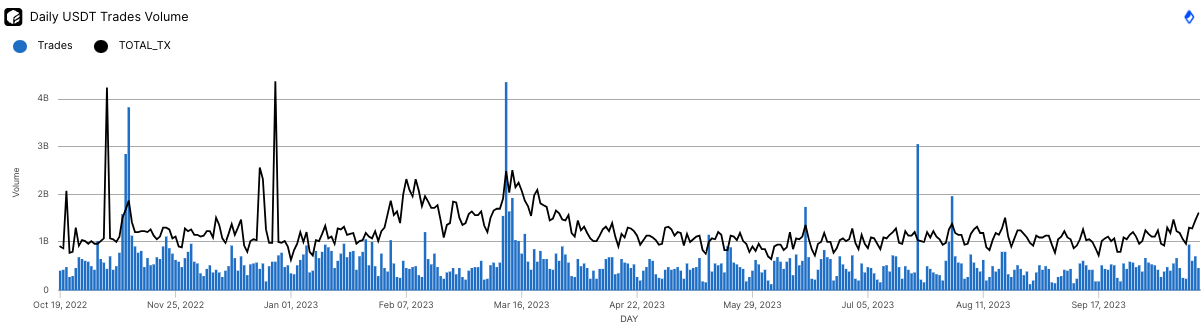

The highest 2 charts on this chapter include comparable knowledge however for several types of USDT transactions. First one is Trades quantity (buying and selling transactions on DEXes) and second one is Personal Transfers (Direct transfers from Consumer A to Consumer B, together with Deposit transactions to CEXes which might be often made by Direct Transfers).

Key Observations

- Finish of November 2022:

- Each charts show important spikes round this time.

- Trades: Massive surge in commerce quantity and transaction rely.

- Direct Transfers: Substantial enhance in personal switch quantity, with a reasonable enhance in transaction rely.

- Mid-March 2023:

- Trades: Distinctive spike in commerce quantity and transaction rely.

- Personal Transfers: A noticeable spike in quantity and a gentle surge in transaction rely.

- Each actions round this era are in step with the March 10-11, 2023 USDC 12% depeg occasion.

- Early June 2023:

- Trades: Vital spike in commerce quantity, elevated transaction rely.

- Personal Transfers: Reasonable enhance in quantity, gentle rise in transaction rely.

- The spikes right here align with the June 15, 2023 USDT 3% depeg occasion.

- Common Observations:

- DEX Trades have extra pronounced spikes in each quantity and transaction rely at key occasions than Direct Transfers.

- Direct Transfers exhibit a steadier quantity with much less drastic fluctuations than Trades.

- Commerce volumes appear to be reactive, probably reflecting market sentiment and reactions to exterior occasions. Alternatively, Personal Transfers appear to symbolize extra constant and maybe deliberate transfers between customers.

- Different Notable Factors:

- Round July 5, 2023, there is a clear spike in Trades however not as pronounced in Personal Transfers.

- The 2 varieties of transactions provide perception into completely different facets of consumer habits. DEX Trades, being extra risky, could point out market sentiment and reactions to information or occasions. In distinction, Direct Transfers appear extra constant and fewer reactionary, probably exhibiting deliberate transactions, remittances, or private CEX deposits for future investments.

- The Personal Switch chart shows a transparent weekly cyclical sample, characterised by:

- Greater Volumes on Weekdays:

- There is a noticeable enhance within the quantity of personal transfers throughout weekdays.

- This might be indicative of business-related transfers or skilled transactions, which usually happen on working days.

- Lower in Quantity on Weekends:

- Volumes drop considerably throughout weekends.

- This development means that fewer personal transfers are made for enterprise or skilled functions throughout weekends.

- Consistency of the Sample:

- This cyclical sample is constant all through the length of the chart.

- Such a recurring sample signifies that the habits isn’t an anomaly however somewhat a mirrored image of normal consumer habits or practices.

- Greater Volumes on Weekdays:

The noticed weekly sample aligns with conventional monetary practices the place enterprise actions, remittances, or skilled transactions predominantly occur on weekdays, whereas weekends see a lull in such actions. It is also indicative of the first consumer base of USDT for personal transfers, the place a good portion may be utilizing it for enterprise or skilled causes.

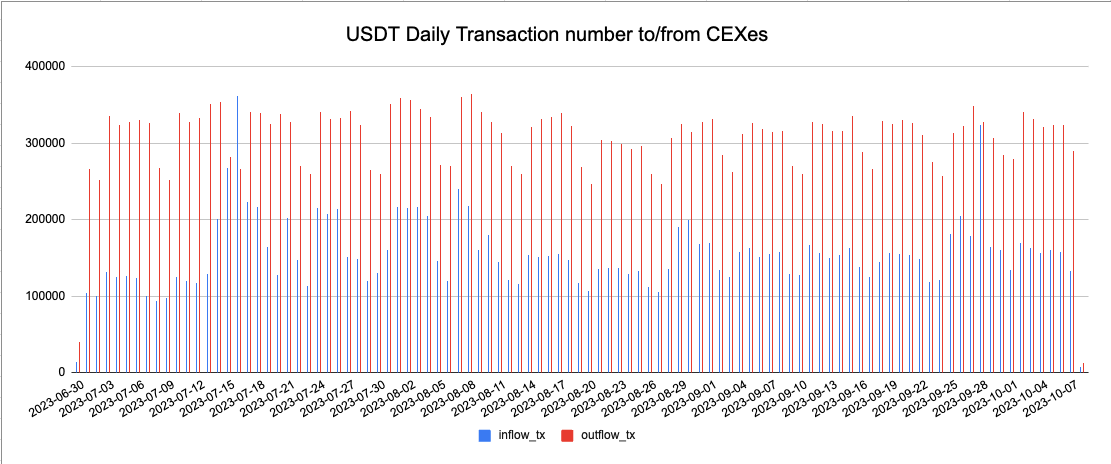

5.4. USDT CEX Flows in Tron

In contrast to in Ethereum, USDT in Tron is generally used for Direct Transfers (95%+ of transactions) leaving simply 5% for DEXes. DEXes in Tron should not broadly used and nearly all of the customers alternate USDT for TRX to pay for transaction commissions. Thus, for functions of this analysis we’ve analyzed:

- In and Out Flows Onto Main CEXes

- The Dataset Used Accommodates Transactions From July 2023 to Oct 2023. (3 Months)

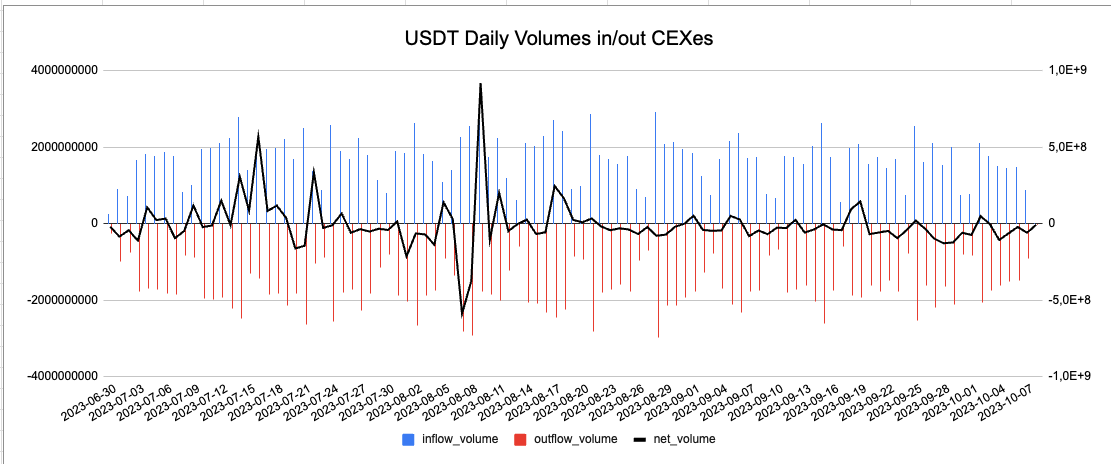

USDT Day by day Volumes in/out CEXes:

- Influx Quantity (Blue Bars):

- Represents the amount of USDT being despatched to centralized exchanges (CEXes).

- There are periodic peaks, indicating days with larger influx than common.

- Outflow Quantity (Purple Bars):

- Denotes the amount of USDT leaving centralized exchanges.

- Just like influx, there are periodic spikes in outflow quantity.

- Internet Quantity (Black Line):

- Exhibits the distinction between influx and outflow.

- It hovers across the zero mark however often dips or rises sharply, indicating important internet outflows or inflows on these days. As an example, across the date 2023-08-14, there is a sharp unfavorable dip indicating extra USDT left the CEXes than entered.

USDT Day by day Transaction quantity to/from CEXes:

- Influx Transactions (Blue Bars):

- Represents the variety of transactions sending USDT to CEXes.

- There is a constant development of influx transactions with some minor each day variations.

- Outflow Transactions (Purple Bars):

- Variety of transactions sending USDT out of CEXes.

- Like influx transactions, the outflow transactions observe a constant development with minor each day fluctuations.

Key Commentary:

- The influx and outflow volumes appear to counterbalance one another more often than not, maintaining the online quantity comparatively steady. This means an energetic and liquid market the place USDT is ceaselessly moved out and in of exchanges.

- The variety of outflow transactions is often twice greater than the variety of the influx transactions, indicating that every deposit is both transformed to property or Fiat on exchanges, or used to separate into no less than 2 smaller parts. On the identical time, assuming the volumes are counterbalanced, then the latter assertion is legitimate.

- The weekly sample noticed on the Day by day Volumes chart, the place there is a noticeably bigger quantity throughout weekdays in comparison with weekends, suggests a number of elements at play:

- Operational Actions: Institutional gamers, OTC desks, or different large-scale operations might need extra actions and transactions through the weekdays, as these are common enterprise hours for many areas.

- Dealer Conduct: Particular person merchants may be extra energetic through the week, with weekends reserved for relaxation or different non-trading associated actions.

6.1. Scope Definition

For this specific analysis, we’ll attempt to analyse the chances to use Journey Rule to the transactions with Stablecoins. In contrast to in Fiat cost methods, blockchain doesn’t have a “cost particulars” discipline nor any details about transacting actors. This makes implementation of Journey Rule problematic if not not possible. However, most Customers depend on third occasion pockets/account suppliers to maintain and function their funds with, and these suppliers (particularly CEXes) do KYC verification. The query is, can this data be queried one way or the other from these suppliers and can it’s sufficient for implementing the Journey Rule?

6.2. Technical Particulars

To begin with, we’ll assume that every Holder has a non-custodial pockets and an account on CEX. On each wallets (accounts) Consumer retains some amount of cash. Account on CEX is verified, which means that Consumer has offered his KYC knowledge and it’s been verified. With a non-custodial pockets, Consumer retains his privateness. No paperwork offered or knowledge obtainable to the supplier of this pockets.

When Consumer A desires to ship Stablecoin to Consumer B, he would possibly select to:

- Ship immediately from CEX account to CEX account of a counterparty

- Ship from his non-custodial account to CEX account of counterparty

- Ship from his CEX account to non-custodial account of counterparty (which is generally prohibited by Phrases and situations of CEXes, that states that customers are allowed to deposit and withdraw to their private addresses solely)

- Make a direct switch from non-custodial pockets to counterparty non-custodial pockets.

By way of Journey Rule utility:

- On this case we have now details about each Consumer A and Consumer B

- On this case we have now details about Consumer B solely

- On this case we have now details about Consumer A solely

- No details about any customers obtainable

However in case we mix case 2 and case 3 (which means, that Consumer A withdrew from CEX to his/her non-custodial pockets, then despatched cash to Consumer B’s CEX Deposit Handle), Journey Rule implementation appears potential as properly.

For functions of this analysis, we’ll think about case 1 and mixed 2+3 case, then give an estimation of transaction quantity and volumes which might be probably appropriate for Journey Rule implementation.

Token transactions and flows for each in addition to some technical particulars and challenges are mentioned within the following chapters.

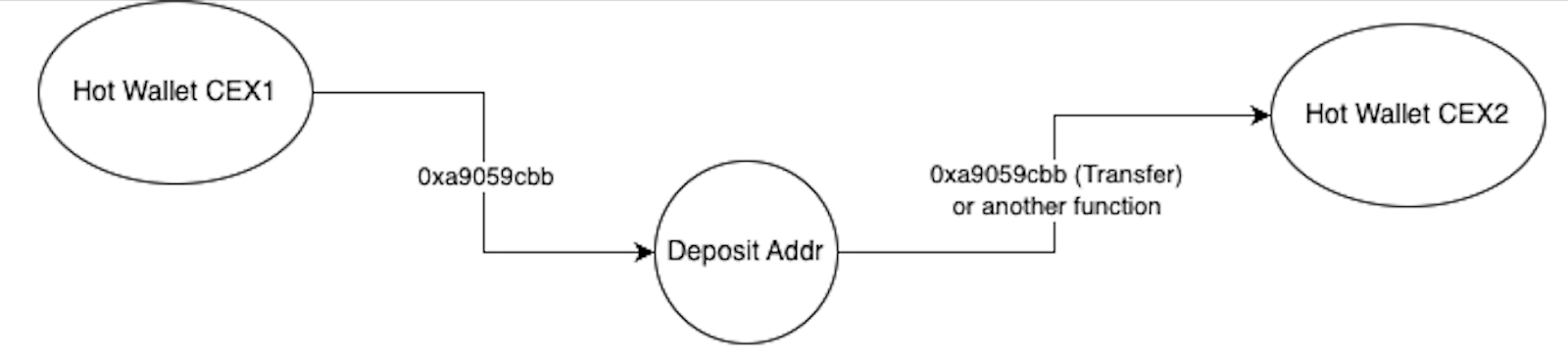

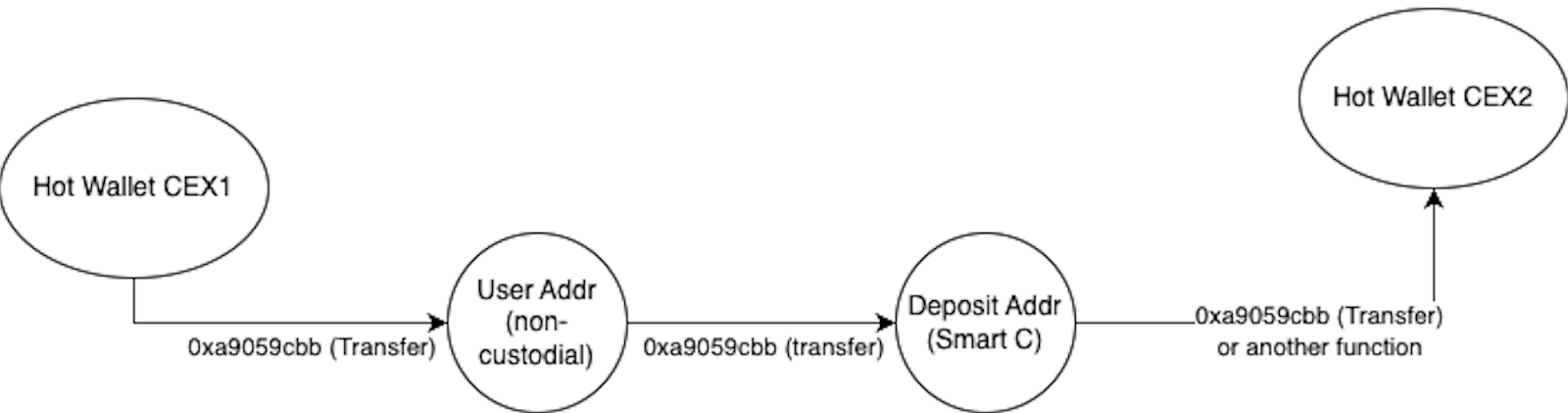

6.2. 1. Case 1. CEX => DepositAddr => CEX

When consumer A points withdrawal from CEX account, it’s truly carried out from a consolidation pockets (i.e. CEX 1 sizzling pockets). What consumer A usually does, is that he supplies a so-called “withdrawal tackle”. This manner the CEX 1 data system understands the place to ship funds. In Case 1 consumer A supplies “Deposit Handle” of consumer B on one other CEX 2.

The habits of the “Deposit Handle” is beneath full management of the CEX data system. It’s designed the best way that it collects deposited funds to a consolidated account (Sizzling Pockets) ASAP. Virtually, inside minutes, however typically it might require 2-3 hours. Additionally, it would transfer precisely the identical quantity that Consumer A deposited after which credit score it to Consumer B account, which can be essential to grasp.

Typically Consumer A sends a small quantity of tokens to Consumer B’s Deposit Handle and waits for Consumer B to verify receival onto his CEX account. Then points switch of excellent quantity. Relying on CEX data system implementation, this leads to 2 transactions issuing from CEX 1 Sizzling Pockets to Deposit Handle, and only one “accumulating” transaction from Deposit Handle to CEX 2 Sizzling Pockets. On this case, it is smart to rely “transfers” primarily based on “assortment” transactions somewhat than “originating” transactions.

By understanding habits patterns above, we are able to make 2 necessary conclusions that may simplify our analysis:

- It is smart to research the final leg (a “accumulating” transaction) by way of switch quantity and date. First leg to be ignored, particularly as a result of the truth that it might end in “duplicates”.

- Time distinction of the two legs might be ignored. “Gathering ASAP” is virtually finished inside minutes after deposit acquired, and undoubtedly throughout the identical enterprise day.

6.2.2. Case 2. CEX => W => DepositAddr => CEX

This case is extra complicated in comparison with the earlier one by way of evaluation. This case consists of an intermediate pockets (W) that belongs to Consumer A. Inside this case the precise circulate is the next:

- Consumer B supplies Consumer A together with his “Deposit Handle” and requests a specific amount of funds (AMT) to be transferred.

- Consumer A opens his/her account on CEX, however as an alternative of doing direct switch to Deposit Handle, s/he decides to withdraw on his personal intermediate tackle W.

- After withdrawal acquired to pockets W, Consumer A initiates switch of requested AMT to Deposit Handle of Consumer B

- When the CEX2 data system detects funds on Deposit Handle, it triggers “accumulating” switch to CEX 2 Sizzling Pockets.

This case consists of three transactions, and the issue is that they may be separated in time and never equal by way of switch quantity. It is vitally arduous to “match” such transactions as a result of this truth. For the needs of this analysis (which is estimation of the transaction quantity {that a} Journey rule might be utilized to), we think about making simplification assumptions that won’t scale back the quantity of transaction detected however could end in “false positives” detections which is a tradeoff we are able to make. The record of assumptions taken:

- We’ll base the calculations on the “accumulating” transaction, identical as we did for Case 1. We think about it’s cheap as a result of:

- Its quantity is outlined by Consumer B who’s requesting cost. That is the one quantity that makes enterprise sense, regardless of how a lot have Consumer 1 initially withdrawn

- Enterprise transaction (Consumer A->Consumer B switch) is taken into account accomplished after “accumulating” transactions are included and confirmed within the blockchain. Then CEX 2 can credit score Consumer B account.

- We’ll match transaction legs primarily based on “addresses” solely. No time or quantity correlation utilized. We think about it’s cheap as a result of:

- When Consumer A withdraws to intermediate Pockets W, it’s often Consumer A’s pockets.

- If it’s not a Consumer A tackle (Consumer C, for instance), Consumer A is aware of precisely who this particular person is. Sending funds to random individuals isn’t sensible.

- Even when Consumer A is a OTC crypto dealer which initiates CEX => W transfers for a lot of his prospects, he is aware of their names too. Vital level is will these prospects transact with somebody on CEX in future (carry out W=> Deposit Handle).

- Consumer A could have some funds on W, so he would possibly withdraw much less funds from CEX1 then Consumer B requested. Or much more funds (in order that will probably be sufficient for extra transfers in future).

- This leads to the truth that CEX1 => W switch quantity could differ loads from initially requested Consumer A->Consumer B switch

- CEX1 => W switch could also be considerably separated in time from precise Consumer A->Consumer B switch we’re excited about.

- Variety of CEX1 => W transfers won’t ever match the variety of carried out enterprise transactions we’re excited about.

- Quantity transferred on Leg 2 (W=>Deposit Handle) matches quantity transferred on Leg 3 (Deposit Handle => CEX 2 Sizzling Pockets) for the explanations mentioned in Case 1. So time and quantity of Leg 2 should not necessary for enterprise transaction evaluation.

By understanding habits patterns above and considering assumptions, we are able to make 2 necessary conclusions that may simplify our analysis:

- It is smart to research the final leg (a “accumulating” transaction) by way of switch quantity and date. First 2 legs are ignored, as a result of the truth that it might end in “duplicates”.

- Time distinction of the legs might be ignored.

- Matching to be finished primarily based on addresses solely.

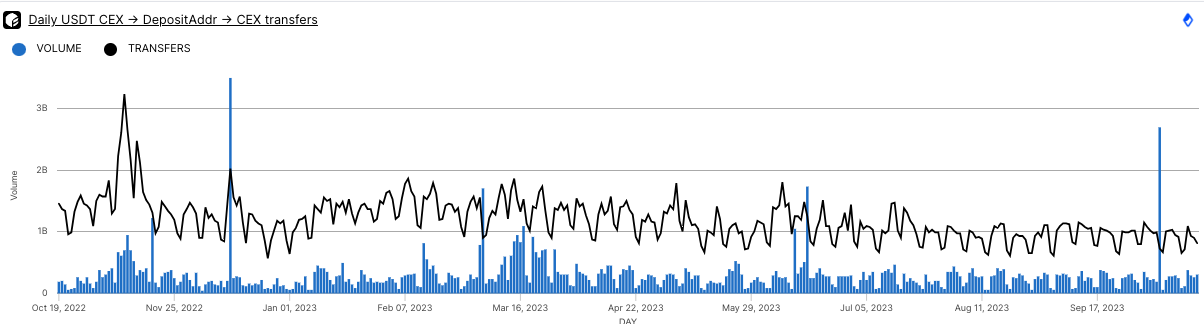

6.3. USDT Journey-Rule succesful transactions in Ethereum

Case 1 (CEX -> DepositAddr -> CEX transfers):

- Quantity (Blue Bars): The quantity peaks are round 2.5B-3B and troughs appear to be round 1B. Averaging these, the estimated common each day quantity is barely above 0.5B USDT.

- Transactions (Black Line): The transaction rely peaks are barely above 10k. Averaging these provides an estimated common each day transaction rely of round 4-5k.

- This case represents roughly 10-15% of complete each day USDT transactions in Ethereum

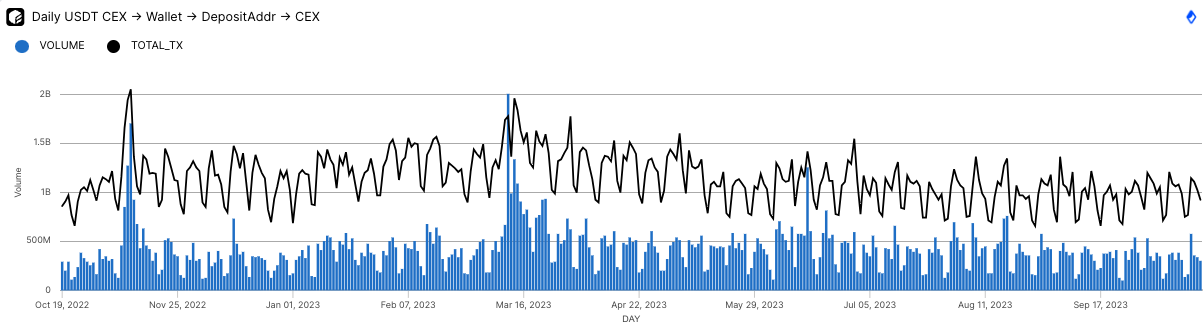

Case 2 (CEX -> Pockets -> DepositAddr -> CEX):

- Quantity (Blue Bars): The quantity peaks round 1.5B-2B and troughs are sometimes above 200M. Averaging the peaks and troughs provides an estimated common each day quantity barely above 1B USDT.

- Transactions (Black Line): The transaction line oscillates with clear weekly patterns, peaking round maybe 15k and dipping to round 8k on the lowest factors. Averaging these provides an estimated common each day transaction rely of round 10k.

- This case represents roughly 7-10% of complete each day USDT transactions in Ethereum

Comparability:

- Quantity: The typical each day quantity for the CEX -> DepositAddr -> CEX pathway is larger, roughly by 200M USDT, in comparison with the CEX -> Pockets -> DepositAddr -> CEX pathway.

- Transactions: The CEX -> Pockets -> DepositAddr -> CEX pathway additionally witnesses a twice larger transaction rely each day, in comparison with the CEX -> DepositAddr -> CEX pathway.

Each charts clearly show a weekly sample, with larger exercise throughout weekdays and decrease exercise throughout weekends, in step with typical crypto buying and selling habits. The direct CEX -> DepositAddr -> CEX transactions have sometimes larger quantity however twice smaller transaction counts in comparison with the transactions that contain an intermediate pockets.

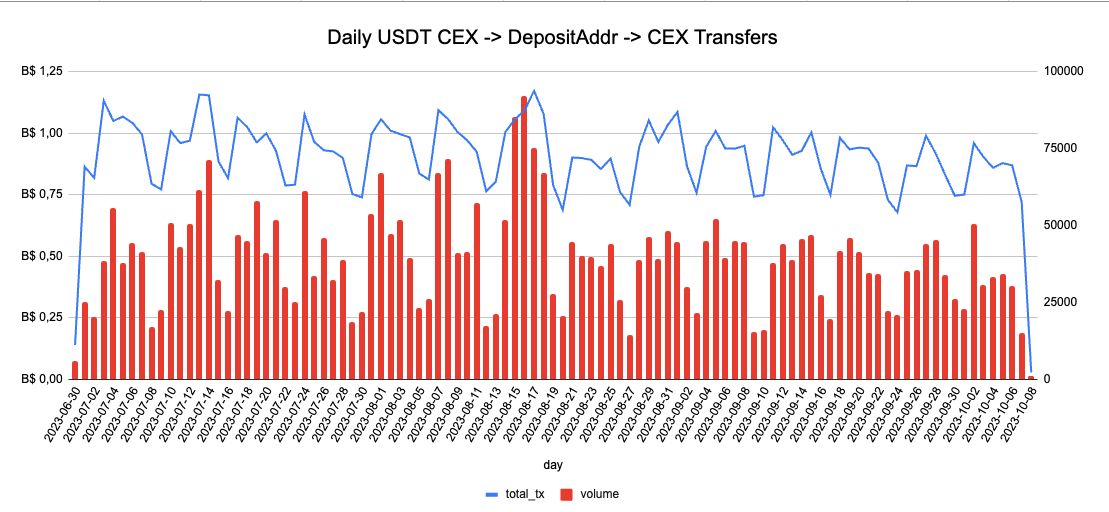

6.4. USDT Journey-Rule succesful transactions in Tron

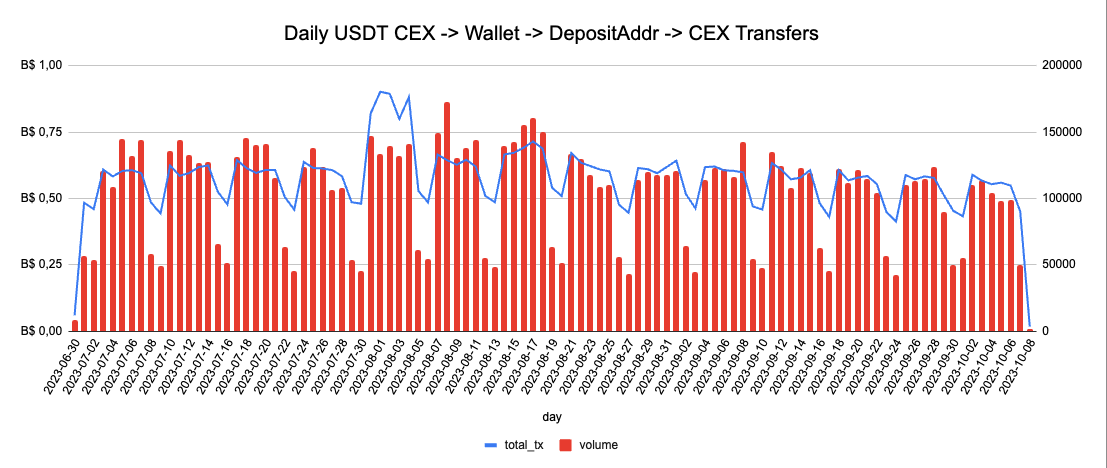

Case 1: CEX->DepositAddr->CEX

- Quantity (Purple Bars):

- Principally fluctuates between 0.25 Billions USDT and BS 1.25.

- Common seems to be round 0.75 Billions USDT.

- Variety of Transactions (Blue Line):

- Ranges roughly between 50,000 and 75,000.

- Common seems to be round 62,500 transactions per day.

- This case represents roughly 4-8% of complete each day USDT transactions in TRON

Case 2: CEX->Pockets->DepositAddr->CEX

- Quantity (Purple Bars):

- Fluctuates roughly between 0.25 Billions USDT and 1.00 Billion USDT, with occasional spikes near 1.00 Billion USDT.

- Common seems to be barely beneath 0.50 Billions USDT.

- Variety of Transactions (Blue Line):

- Oscillates roughly between 50,000 and 200,000, averaging someplace across the center.

- Common appears near 125,000 transactions per day.

- This case represents roughly 4-5% of complete each day USDT transactions in TRON

Comparability:

- Quantity: The second chart (CEX->DepositAddr->CEX) tends to have the next common each day quantity at round 0.75 Billions USDT in comparison with the primary chart’s common of barely beneath 0.50 Billions USDT.

- Transactions: The primary chart (CEX->Pockets->DepositAddr->CEX) has the next variety of transactions per day, averaging round 125,000, whereas the second chart averages at about 62,500.

Each charts certainly have a weekly sample, possible as a result of market exercise being decrease on weekends and better on weekdays.

7.Conclusions

- In contrast to Tron, Ethereum has considerably greater DEX utilization. Tron retains its place on the OTC market as an alternative.

- In each Ethereum and Tron USDC exhibits a recurrent weekly sample of actions, particularly on Direct Transfers. Such “background” actions don’t correlate a lot with buying and selling occasions and market situations, thus are impressed not by speculations on CEXes/DEXes, however by one other kind of consumer case (and subsequently – companies)

- Assuming CEXes are all regulated, with correct KYC and compliance procedures in place, Journey Rule might be enforced for not more than 20% and 12% transactions for USDT in Ethereum and Tron correspondingly.

- This can be a prime estimate as a result of assumptions taken on this analysis, sensible outcomes will give decrease numbers,

- This requires a “communication layer” constructed between CEXes, which may be in numerous jurisdictions.

- The rise of Privateness Preserving protocols will scale back effectivity of open ledger primarily based surveillance. Such protocols are likely to combine KYC suppliers these days, and carry out KYC for his or her customers. However they don’t seem to be able to offering any data that binds Enter and Output from their swimming pools and thus, can’t implement Journey rule technically.